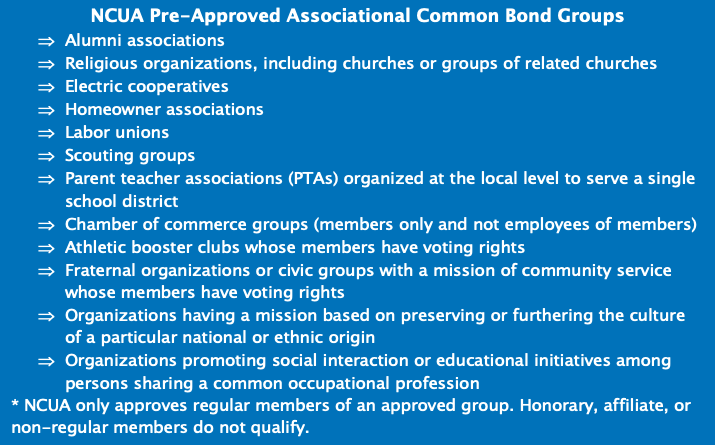

As federal credit unions seek to expand their fields of membership, more and more credit unions are adding associations to their fields of membership. The American Consumer Council is the most popular association credit unions have leveraged to open their fields of membership up to anyone who joins the council. But if you want to use a different association or your credit union’s foundation, what’s your best bet to get approved by the NCUA?

According to the NCUA’s Field of Membership Chartering Manual, the NCUA must approve the amendment to Section 5 of a credit union’s charter, which defines the field of membership. The organization and the credit union must reach an agreement between the two organizations. Second, the credit union must be a multiple common bond credit union or qualify to change its common bond from a single associational common bond to a single occupational common bond or multiple common bond.

A federal credit union requesting a common bond expansion must submit an Application for Field of Membership Amendment. They should use either NCUA 4015-EZ (for organizations with up to 3,000 employees or members), 4015-A (for organizations with between 3,001 and 5,000 employees or members), or NCUA 4015 (for organizations with more than 5,000 employees or members) to the NCUA Office of Credit Union Resources and Expansion to document that the associational common bond requirements are met. An authorized credit union representative must sign the request.

The association seeking membership must also be within the federal credit union’s service area and can “reasonably be served” by a service facility (a place where shares are accepted, loan applications are accepted, or loans are disbursed), including shared branches in which the credit union participates if the credit union has a direct or indirect ownership interest in the shared branch or the shared branch is “local to the credit union.” Typically, a group can be reasonably served by a facility if the group’s headquarters, “paid from” location or a majority of members are within 25 to 30 miles of a branch but there are some exceptions.

In addition to an NCUA 4015 or 4015-EZ, the amendment package must include a letter signed by an authorized representative of the group to be added, and when possible, on the group's letterhead stationary. The regional director may accept other documentation or certification as deemed appropriate. This letter must indicate:

- How the group shares the credit union’s associational common bond;

- That the group wants to be added to the applicant federal credit union's field of membership;

- Whether the group presently has other credit union service available; and

- The number of persons currently included within the group to be added and their locations.

- The most recent copy of the group's charter and bylaws or equivalent documentation.

- If the group is eligible for membership in any other credit union, documentation must be provided to support inclusion of the group under the overlap standards.

For organizations not on NCUA’s pre-approved list, the NCUA applies a “totality of the circumstances test,” meaning no one factor can determine an association’s appropriateness by NCUA’s standards, but the agency does focus more on factors 1 through 4. The test comprises these factors:

- Whether the association provides opportunities for members to participate in the furtherance of the goals of the association;

- Whether the association maintains a membership list;

- Whether the association sponsors other activities;

- Whether the association's membership eligibility requirements are authoritative;

- Whether members pay dues;

- Whether the members have voting rights; to meet this requirement, members need not vote directly for an officer, but may vote for a delegate who in turn represents the members' interests;

- The frequency of meetings; and

- Separateness, in which the NCUA reviews if there is corporate separateness between the group and the federal credit union. The group and the federal credit union must operate in a way that demonstrates the separate corporate existence of each entity. Specifically, this means the federal credit union and the group's respective business transactions, accounts, and corporate records are not intermingled.

Submitted amendments are then reviewed by the NCUA Office of Credit Union Resources and Expansion. CURE will also consider the economic advisability of a common bond expansion, including the impact on the applicant credit union’s operations and financials, as well as the impact to other credit unions the field of membership amendment would overlap. This information will primarily come from NCUA’s examination process and financial and statistical reports, but in some cases, more data is required.

While the federal credit union’s financial and operational situation are a factor, updating the field of membership may improve poor performance, and therefore, could be approved. In this case, the applicant credit union must document that the expanded field of membership is in the best interest of the members and will not increase the risk to the National Credit Union Share Insurance Fund, according to the NCUA Chartering and Field of Membership Manual.

Once approved, the credit union will be issued an amendment to Section 5 of its charter. However, if the field of membership amendment is not approved, the applicant will be informed in writing why it was not approved; recommendations for gaining approval, as appropriate; and procedures for appealing the decision.

Adding an association to your charter comes down to getting the NCUA application right. CUCollaborate handles the documentation and the approval process from start to finish. Talk to us about adding an association.